Previous Story

Bancolombia Says Colombia’s TES Rally Outruns a Fiscal Picture Its Own Government Plays Down

Posted On June 30, 2026

Comment: 0

Tag: abelardo de la espriella, afp, banco de la republica, bancolombia, budget execution, Colombia bond market, Colombia economy 2026, commercial banks, emerging markets, Federal Reserve, Fiscal Deficit, FOMC, Grupo Cibest, inflation Colombia, Laura Clavijo, Marco Fiscal de Mediano Plazo, mfmp, monetary policy, pension funds, Presupuesto General de la Nación, public debt, sovereign risk, tes, total return swap, US Treasuries

Colombia’s peso-denominated government bonds rallied across the entire yield curve over the past month, lifted by the close of a contentious presidential election and a calmer reading of global risk, but the research arm of Bancolombia (NYSE: CIB, BVC: BCOLOMBIA) cautions that the gains sit on top of a fiscal outlook the government’s own framework treats too optimistically. The assessment comes from the bank’s Monthly Public Debt Market Report for June, prepared by the Dirección de Investigaciones Económicas, Sectoriales y de Mercado (Directorate of Economic, Sector and Market Research) of Grupo Cibest, the financial holding group that owns Bancolombia.

A mixed month for US Treasuries

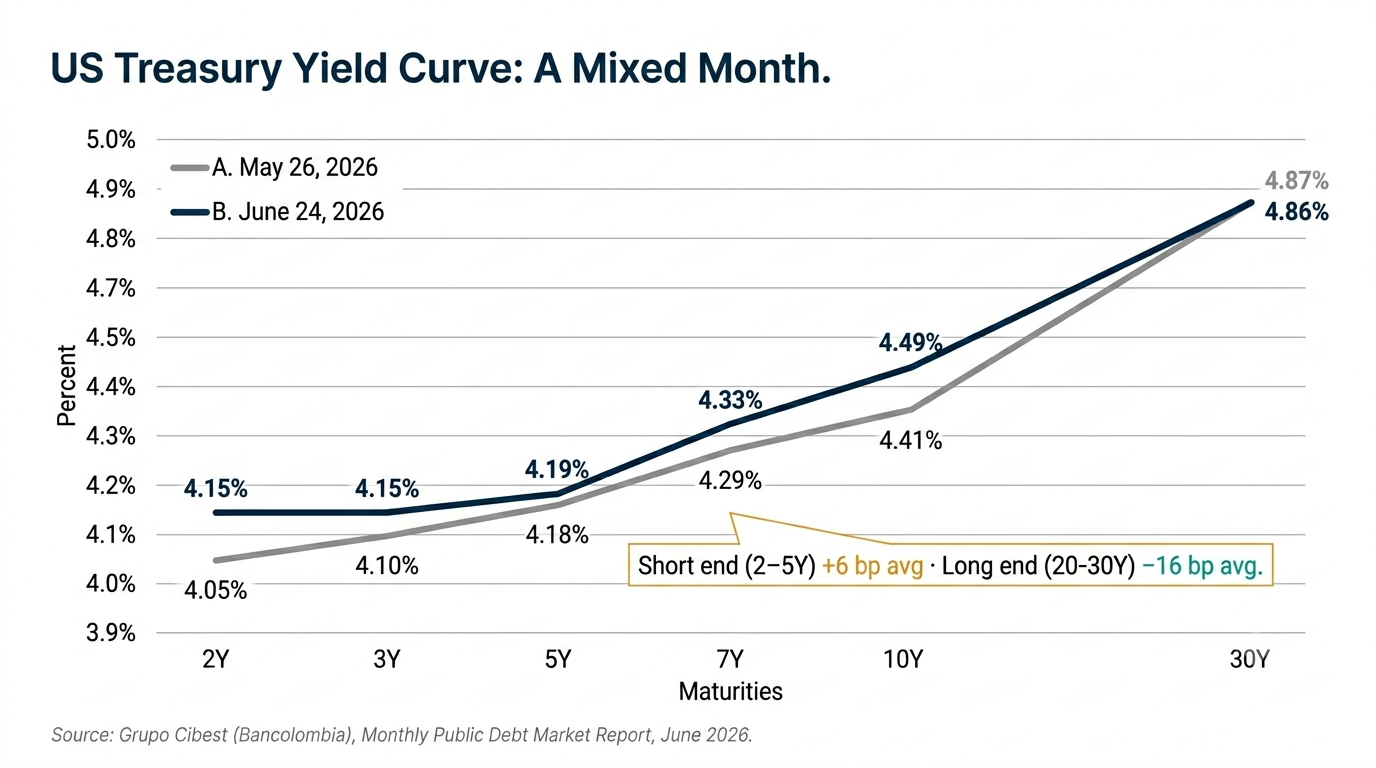

Between May 26 and June 24, the US Treasury yield curve moved in two directions, according to the report. Yields on maturities between two and five years rose by an average of 6 basis points, while the 20- and 30-year segments fell by an average of 16 basis points. The research team tied the move to a communiqué indicating that the US and Iran had reached a memorandum of agreement during the final week of the period, aimed at extending the current ceasefire. Oil prices swung on mixed headlines through the period, and markets also took in inflation data that landed in line with the analyst consensus. In the US labor market, the report noted a stable unemployment rate alongside a significant increase in job openings.

Against that backdrop, the Federal Open Market Committee voted unanimously to hold the federal funds rate in the 3.50% to 3.75% range, a decision the bank flagged as the first without dissent in the past year and consistent with the Federal Reserve‘s prudent stance. The accompanying projections revised the 2026 growth outlook lower and the 2028 outlook higher; the unemployment forecast was cut only for 2026, while the inflation view was revised upward.

Cross-border demand for US debt strengthened. The US Treasury reported that foreign investors made net purchases of long-term bonds of $50.5 billion USD in April, the highest figure since November 2025. Private investors accounted for $30.8 billion USD of net buying in long-term Treasuries, a moderation from the pace seen in March. By geography, the net purchases concentrated in the United Kingdom and Japan, at $26 billion USD and $14.7 billion USD respectively, while investors domiciled in Canada were the largest net sellers as the country’s foreign reserves fell by $42.3 billion USD, followed by Norway and Korea.

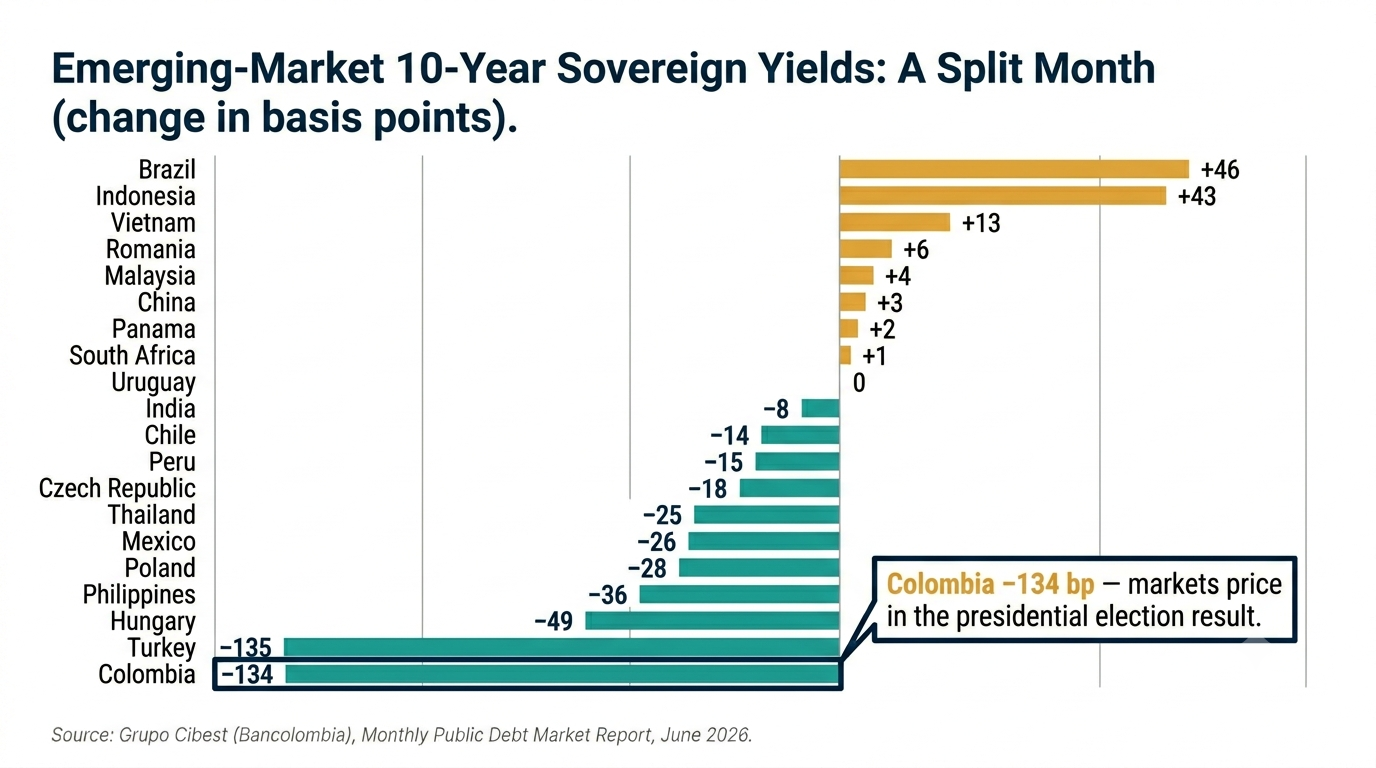

Across emerging markets, 10-year sovereign yields moved unevenly over the month as investors responded to country-specific factors. Brazil led the increases at 46 basis points, followed by Indonesia at 43, Vietnam at 13 and Romania at 6, while Chile, Peru, India, Poland and the Czech Republic recorded declines. The report highlighted a 134-basis-point drop in Colombia, which it attributed to the market’s reaction to the first- and second-round presidential results that left Abelardo de la Espriella as president-elect for the 2026–2030 term.

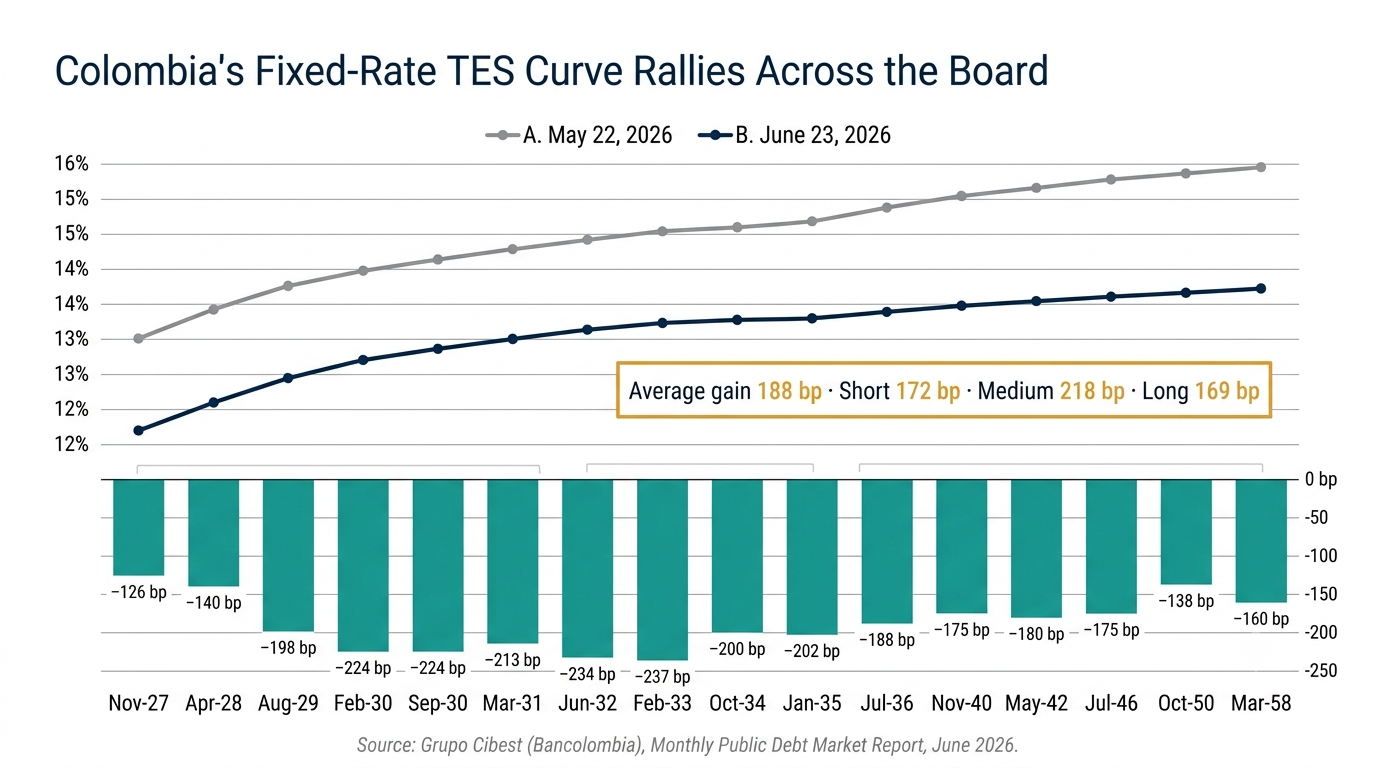

The TES curve gains across the board

At home, the fixed-rate TES curve — Colombia’s peso-denominated treasury bonds — appreciated along its entire structure. Between May 22 and June 23 the curve gained an average of 188 basis points as yields fell across every segment: the short end (one to four years) by 172 basis points, the middle (five to nine years) by 218, and the long end (more than 10 years) by 169. The report attributed the move on the external side to the evolution of the Middle East conflict and the expectation of de-escalation agreements, and to the Fed’s decision to hold rates, which reinforced a cautious tone. Locally, it said the rally responded mainly to the first-round presidential result and held through the following three weeks, producing a stronger appetite for local debt.

An optimistic fiscal frame the bank questions

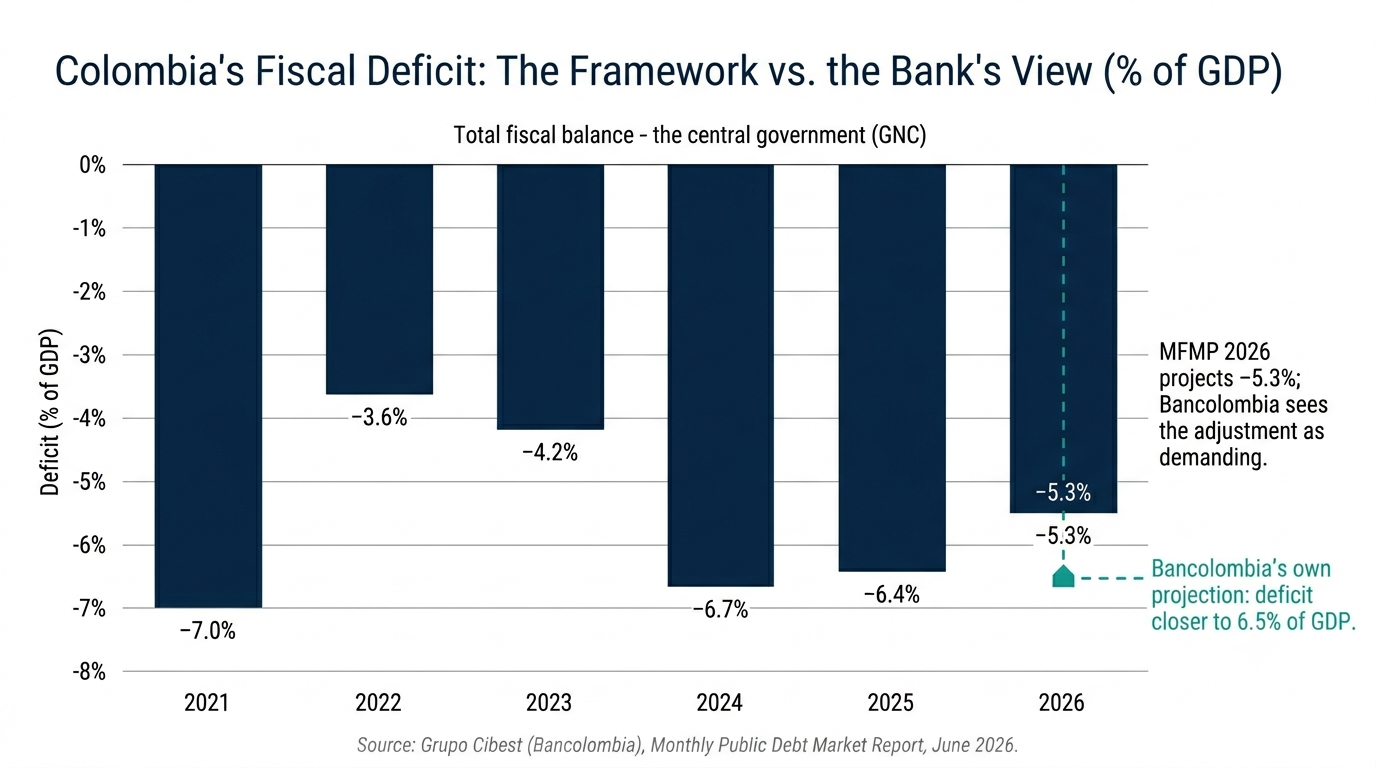

The report said the fiscal deficit would narrow in 2026 according to the figures in the Marco Fiscal de Mediano Plazo (Medium-Term Fiscal Framework). After its most recent update, the bank wrote, the National Government presented an optimistic outlook that does not fully incorporate the fiscal fragilities for 2026. The framework projects a deficit of 5.3% of GDP and a primary deficit improving to 2.1% of GDP. The research team countered that, while debt-management operations have improved the structure of debt service, they have been insufficient to halt the structural growth of interest payments, which would reach 3.9% of GDP in 2027 and remain above 4% in the following years. It added that debt reduction could be constrained by new financing needs in a low-liquidity environment, and that the framework itself acknowledges the need for an additional revenue adjustment of close to 1.6% of GDP to stabilize the debt.

The bank’s own outlook is more cautious than the government’s headline number. In its factor-by-factor view of the coming month, the research team described the fiscal panorama as a continuing source of concern and said the projected 2026 adjustment looks demanding, with revenue and spending pressures pointing to a deficit closer to 6.5% of GDP. Colombia lost a notch of its sovereign credit rating earlier this year, when S&P Global Ratings cut the country to BB- on fiscal concerns.

On budget execution, the report said the Presupuesto General de la Nación (General Budget of the Nation) had reached 46.7% of accumulated appropriations through May. Commitments under the budget totaled $259.8 trillion COP year-to-date, 5.5 percentage points above the same period of 2025. By component, investment led with 58.1% execution, followed by debt service at 50.0% and operating expenses at 43.1%. In terms of effective execution, accrued obligations through May reached $187.2 trillion COP, or 33.7% of appropriations, while payments stood at $185.7 trillion COP, or 33.4%.

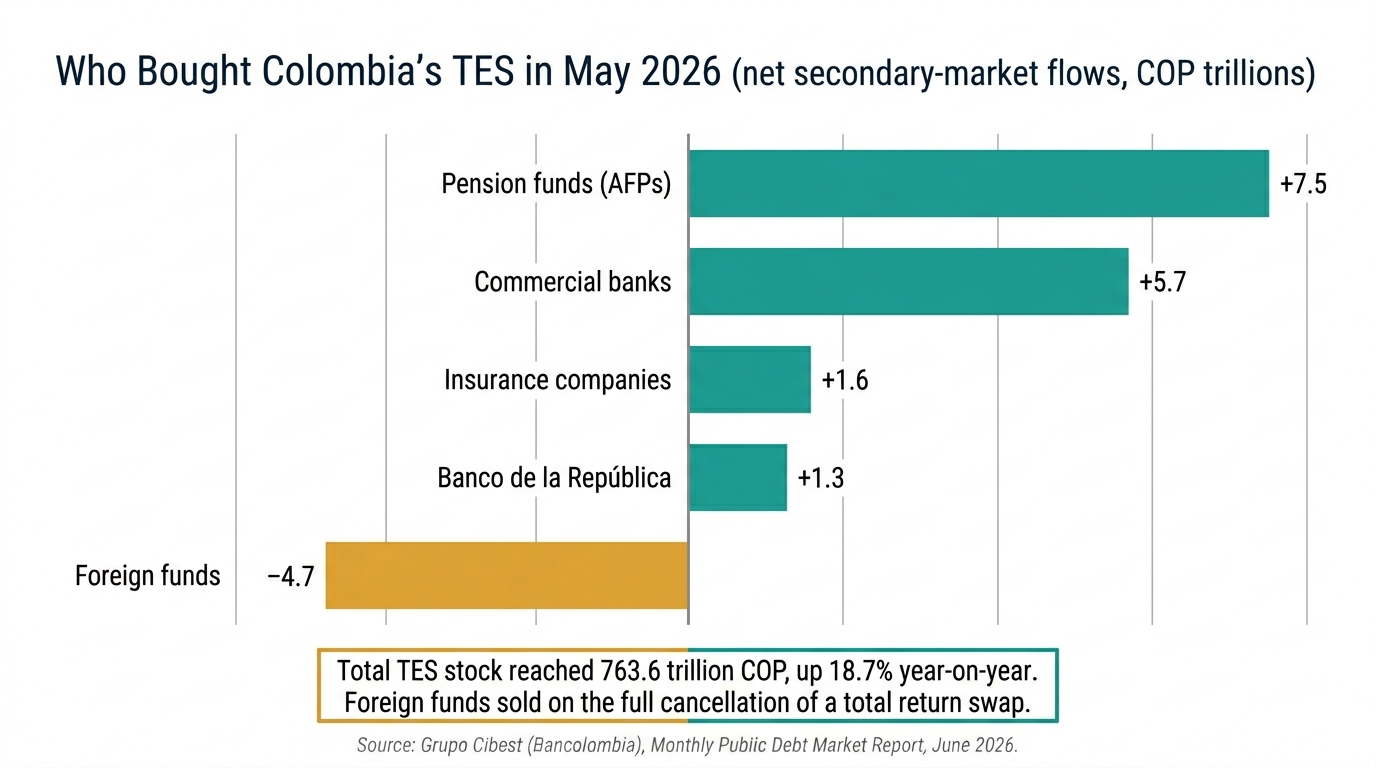

Pension funds and banks lead TES buying

In May, pension fund managers (AFPs) and commercial banks led the month’s TES purchases, the report said. The total stock reached $763.6 trillion COP, an annual increase of 18.7% and a 1.9% gain over April. In the secondary market, net purchases came to $14.1 trillion COP, driven mainly by AFPs at $7.5 trillion COP, commercial banks at $5.7 trillion COP, insurance companies at $1.6 trillion COP and the Banco de la República at $1.3 trillion COP. Foreign funds were the largest net sellers, with a balance of -$4.7 trillion COP, a result the report attributed to the full cancellation during the month of a total return swap (TRS).

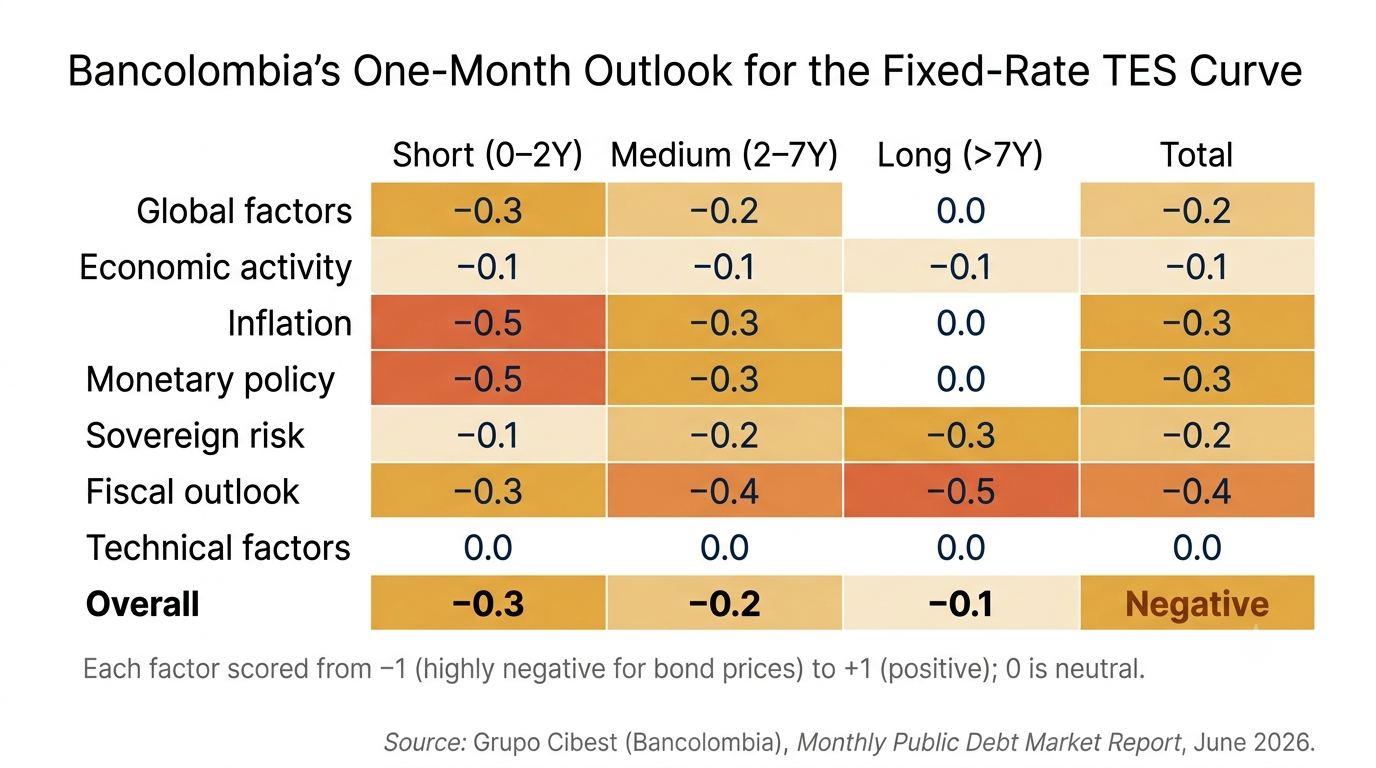

A negative tilt for the month ahead

Looking to the next month, the research team rated the balance of factors for the fixed-rate TES curve as negative overall, with the most negative readings at the short end. It pointed to a Federal Reserve holding a restrictive stance amid persistent inflation and a resilient labor market, and to external uncertainty tied to the Middle East and energy prices. On the domestic side, it noted that the economy grew 2.5% year-on-year in the first four months — less dynamic than initially expected after a retreat in primary activities — while public spending and private consumption should continue to support activity through the rest of the year.

The bank flagged inflation and monetary policy as the clearest pressures on local bonds. Annual inflation has stalled in its convergence toward the Banco de la República’s 2.0%–4.0% tolerance range and has begun to accelerate on high indexation and economic momentum, with gasoline-price adjustments, costlier fertilizers and an El Niño event capable of adding further pressure and putting inflation near 6.4% at year-end. With expectations rising, the policy rate stands at 11.25% and, the report said, could reach 12.00% at the June meeting and approach 12.75% in the second half of 2026 as the central bank works to anchor expectations. Set against those headwinds, the bank noted that Colombia’s sovereign risk premium fell over the month to below the Latin American average following the end of the electoral process, even as questions about the sustainability of public finances remain.

The report was prepared by the Directorate of Economic, Sector and Market Research of Grupo Cibest, led by Laura Clavijo, drawing on data from the Federal Reserve, the US Treasury, the Ministry of Finance and Public Credit (Ministerio de Hacienda y Crédito Público), the Banco de la República, LSEG Workspace and JP Morgan.