Previous Story

Grupo Cibest Cuts Colombia’s 2026 Growth Forecast to 2.6% as Inflation and Fiscal Risks Mount

Posted On July 13, 2026

Comment: 0

Bank sees rates at 12.75% and a deficit near 6.5% of GDP in 2026

Grupo Cibest, the Medellín-based financial holding company that owns Bancolombia (NYSE: CIB), has cut its 2026 economic growth forecast for Colombia to 2.6% from 2.9%, warning that the economy is losing traction as its main growth engines tire, inflation reaccelerates, and the public finances deteriorate.

The downgrade came in the bank’s mid-year update of economic projections, prepared by its economic, sectoral, and market research division under research director Laura Clavijo. The team framed 2026 as a year of macroeconomic stabilization shadowed by mounting medium-term challenges, with risks tilted to the downside for growth and to the upside for inflation and interest rates.

Growth concentrated in consumption and public spending

According to the report, gross domestic product expanded 2.2% year over year in the first quarter of 2026, and just 0.6% from the previous quarter in seasonally adjusted terms, undershooting the bank’s earlier expectations. Grupo Cibest attributes the slowdown to the exhaustion of the two drivers that carried the post-pandemic recovery: private consumption and public spending. The bank had earlier shown Colombia’s economy accelerating into the second quarter, but its NowCast model has since held growth estimates near 2.6%.

“In sum, the Colombian economy moves through 2026 in an environment of converging risks that challenges progress on structural gains.” — Grupo Cibest economic research team

The research team expects private consumption growth to ease to 2.8% in 2026 from 3.5% in 2025, pressured by high interest rates and inflation, even as remittances and a resilient labor market continue to support household spending. Public spending is projected to grow about 6.0%, after 8.4% in 2025, helped by the activation of the escape clause in the Regla Fiscal (Fiscal Rule), which gives the government more room to run an elevated deficit. Fixed investment is forecast to rise 3.5%.

The expansion would be uneven across sectors. Mining is expected to keep contracting, falling about 5.3% on lower coal and oil extraction, while construction declines 1.6% amid high financing costs and a difficult housing market. Manufacturing growth depends largely on household demand, and services, led by entertainment, remain the principal driver of the economy. On the external side, the bank sees exports growing 2.9% and imports 6.3%, narrowing the goods trade gap relative to prior forecasts.

Inflation reaccelerates, central bank turns more restrictive

The report describes a fresh setback in the inflation cycle that will slow convergence toward the central bank’s target. Consumer inflation rose to 5.84% in May from 5.10% at the close of 2025, and Grupo Cibest expects it to climb to roughly 6.4% by the end of 2026, driven by widespread price indexation, this year’s minimum-wage increase, and inflationary inertia. A strong El Niño event, recently declared, poses an additional upside risk through food and energy supply shocks, with the bank estimating a severe episode could add 0.7 to 1.9 percentage points to annual inflation. Pressures are most persistent in services, which make up close to half of the consumption basket.

Against that backdrop, the Banco de la República (Colombia’s central bank) has interrupted its rate-cutting cycle and shifted to a more contractionary stance, having already moved to lift rates earlier in the year amid inflationary pressure. Grupo Cibest projects the policy rate will reach 12.75% by the end of 2026, an additional 150 basis points from current levels and a level not seen since February 2024, and stay elevated through much of 2027 before a gradual normalization that would bring it toward 7.0% by 2030. Twelve-month inflation expectations stand at 5.5% and 24-month expectations at 4.3%, both above the central bank’s 2.0% to 4.0% tolerance range.

Fiscal deterioration the main vulnerability

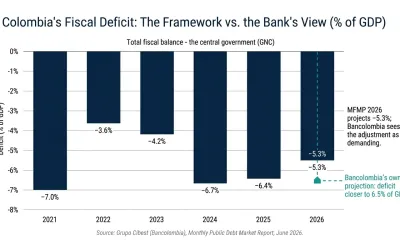

Grupo Cibest singles out the fiscal front as the principal source of macroeconomic vulnerability. The bank projects a Central National Government deficit of about 6.5% of GDP in 2026, above the 5.3% the Ministerio de Hacienda (Finance Ministry) laid out in its Marco Fiscal de Mediano Plazo (Medium-Term Fiscal Framework) in early June. The research team considers the official framework optimistic, particularly on inflation and primary spending, and estimates the primary deficit will near 3.2% of GDP rather than the official 2.1%.

Revenue performance has been strong: tax collection reached roughly 139.3 trillion COP by May, up 9.4% year over year and surpassing the targets set by the national tax authority, DIAN. But high budget execution and spending rigidity have made the required adjustment difficult, with commitments through May reaching 259.8 trillion COP, about 27.5 trillion COP above plan. To hit its fiscal target, the government would need to cut some 33.2 trillion COP from the 2026 budget, which the bank calls improbable given recent execution. As a result, gross public debt could rise to 65.9% of GDP, approaching 66%, and the heavier reliance on local-currency bond issuance to cover financing needs would keep upward pressure on yields. Grupo Cibest argues the absence of structural adjustment reinforces the need for a tax reform raising close to 1.6% of GDP to stabilize the debt trajectory. The fiscal picture echoes recent warnings from rating agencies, including Fitch’s view that revised deficit targets heighten fiscal uncertainty.

External accounts improve, peso firms

The external picture is more favorable. The bank estimates the current account deficit will narrow to 2.3% of GDP in 2026 from 2.4% in 2025, well below the pre-pandemic decade average, before widening gradually toward 3.3% over the medium term. The improvement reflects stronger exports, favorable commodity prices led by oil, and record remittance inflows that have climbed to near 4.0% of GDP. The bank sees Brent crude averaging $86 USD per barrel in 2026.

The Colombian peso has appreciated 9.2% so far this year, supported by capital flows returning to Latin America, the central bank’s rate-hike cycle, strong remittances, and expectations around the change of government. Grupo Cibest revised its average exchange rate forecast down to 3,635 COP per dollar and expects the currency to trade between 3,400 and 3,650 COP per dollar in the second half, with the trajectory hinging on credible signals of fiscal consolidation. The bank had earlier flagged a firmer peso after the currency’s appreciation in April.

Stabilization, with conditions

For the medium term, Grupo Cibest expects growth to stabilize around potential, near 2.6% to 2.7% annually through 2030, with the unemployment rate averaging 9.0% in 2026, and credit growth moderating to 1.9% in real terms while loan quality holds near a 3.9% non-performing ratio. The bank notes that a new administration, after Colombia confirmed a change of government on June 21, could improve investor expectations to the extent it advances a more market-oriented agenda, though it cautions that high interest rates will continue to weigh on private investment in capital-intensive sectors such as mining and construction.

The report ties its outlook to the persistence of converging risks. “In sum, the Colombian economy moves through 2026 in an environment of converging risks that challenges progress on structural gains,” the research team wrote, pointing to the loss of momentum in growth drivers, persistent inflationary pressures, significant fiscal deterioration, and more restrictive financial conditions.