Previous Story

Colombia’s Peso Rallies 7.4% in June as the Election Result Overrides a Hostile Global Backdrop

Posted On July 7, 2026

Comment: 0

Tag: abelardo de la espriella, banco de la republica, bancolombia, Bank of Japan, Brent Crude, carry trade, Colombia economy 2026, Colombia presidential election 2026, colombian peso, Dollar Index, dxy, european central bank, Exchange Rate, Federal Reserve, Fiscal Deficit, Grupo Cibest, interest rate, ivan cepeda, jp morgan, Laura Clavijo, ministry of finance, monetary policy, oil prices, tes, USDCOP

Bancolombia sees the peso at 3,440-3,580 per dollar in July.

The Colombian peso was the standout performer among global currencies in June, appreciating 7.4% on the month even as the US dollar broadened its strength and oil prices dropped sharply. According to the Monthly FX Market Report published by the research arm of Bancolombia (NYSE: CIB, BVC: BCOLOMBIA), the peso closed the month at 3,415.25 per dollar, a gain of 274 pesos over the period. The report was prepared by the Economic, Industry and Market Research Area of Grupo Cibest, the financial holding group that owns Bancolombia.

The move ran against the grain of the month’s external drivers. The dollar index (DXY) strengthened 2.3% and Brent crude fell 20.7%, a combination that would ordinarily weigh on a commodity-linked emerging-market currency. Instead, the peso rose on domestic factors tied to Colombia’s presidential election, tracking a rally in local assets that priced in a higher probability of a market-friendly outcome.

The election set the tone

The peso’s appreciation was in line with the rally in local assets that followed the first round of the presidential election, which raised the perceived odds of a right-wing candidate’s victory, the report said. That pattern — commonly observed across the region — limited any upside for the dollar after the second round. Abelardo de la Espriella was elected to govern for the 2026–2030 term, winning 49.63% of the vote, or 12,960,166 ballots, in the tightest race since 1994. Iván Cepeda secured 48.67%, or 12,708,312 votes, and conceded after the official tally was released.

Overseas voting favored de la Espriella, at 64%, the report noted, while domestically he drew strong support in central regions, including Norte de Santander at 76%, Casanare at 69%, Santander at 65%, Antioquia at 64% and Huila at 61%. Voter turnout reached a historic high of 26.3 million participants, or 63.6% of the electorate, with blank votes marginal at 1.6%.

Markets reacted positively to the shift in the government’s political spectrum. JP Morgan recommended maintaining long positions in TES, Colombia’s peso-denominated treasury bonds, according to the report; the bank also held a neutral stance on the peso and closed its short positions against the Brazilian real and the Mexican peso. Through the month the dollar traded between 3,385 and 3,613 pesos, with average intraday volatility of 44 pesos.

“The Colombian peso appreciated in June on idiosyncratic factors, defying the global backdrop.” – Economic, Industry and Market Research Area, Grupo Cibest (Bancolombia), Monthly FX Market Report, June 2026

The central bank resumes its hiking cycle

Following a pause in April, the Banco de la República, Colombia’s central bank, resumed its tightening cycle and, by majority decision, raised its policy rate by 75 basis points to 12%. The report characterized the decision as reinforcing a more restrictive stance amid persistent inflationary pressures, in an environment where tensions between the bank and the Executive appeared to have eased. That rate level, it said, is supportive of long peso positions.

Major central banks abroad kept a cautious posture. The Federal Reserve unanimously held its policy rate in the 3.50% to 3.75% range and revised its expected rate path higher, with the median projection for 2026 pointing to a 25-basis-point increase. The European Central Bank raised its policy rate by 25 basis points to 2.25%, a level not seen since April 2025, while the Bank of Japan lifted its rate by 25 basis points to 1.0%, its highest since 1995.

Defying the global backdrop

The peso appreciated on idiosyncratic factors even as the broader environment turned less favorable, the report said. Markets closely tracked the Middle East conflict, where the US and Iran reportedly reached a peace memorandum that included the reopening of the Strait of Hormuz, the lifting of the US blockade on Iranian ports, the release of frozen Iranian assets and a 60-day window to discuss Iran’s nuclear program. In that context Brent prices fell 20.7%, closing at $72.97 USD per barrel, while WTI settled at $69.60 USD, down 20.3% on the month. The report cautioned that the normalization of trade flows would be gradual, citing reported Israeli attacks and episodes of tension between the US and Iran that leave a definitive peace uncertain. Gold prices fell 11.8%, closing at $4,023 USD per ounce, on shifting rate expectations and reduced demand for dollar-denominated safe-haven assets.

The dollar index, meanwhile, strengthened 2.3%, driven by expectations of higher-for-longer US interest rates. Even so, the peso outpaced its regional and developed-market peers by a wide margin. Among the currencies that gained against the dollar in June, the Swedish krona rose 5.2%, the Chilean peso 3.7%, the Swiss franc 3.5%, the Canadian dollar 2.9%, the Brazilian real 2.6%, the Japanese yen 2.1% and the euro 2.1%, while the Mexican peso and the Peruvian sol added 0.9% and 0.5%, respectively. The Colombian peso’s 7.4% advance left the field behind.

The month ahead

The research team expects the dollar to trade within a range of 3,440 to 3,580 pesos in July, against a backdrop of elevated global uncertainty. Markets are likely to maintain a constructive bias following the change in government, the report said, though cabinet appointments and signals on fiscal consolidation from the incoming administration will be key to sustaining the trend.

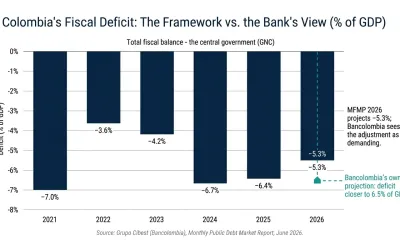

The bank framed the risks in two directions. Upside risks for the dollar remain linked to the deterioration of public finances: the Ministry of Finance has explicitly highlighted the need to strengthen fiscal revenues through an adjustment of around 1.6% of GDP, a scenario the report said would be necessary to stabilize net debt below 60% of GDP over the next decade. Colombia’s fiscal trajectory has already drawn scrutiny from ratings agencies, with S&P Global Ratings cutting the country to BB- earlier this year on fiscal concerns. Downside risks for the dollar, by contrast, persist in connection with carry-trade strategies, particularly as the central bank resumes its rate-hiking cycle and widens the rate differential that rewards holders of peso assets.

The Monthly FX Market Report was prepared by the Economic, Industry and Market Research Area of Grupo Cibest, with contributions from International FX and Rates Analyst Maria Paula Gonzalez, Chief Economist Laura Clavijo and Macroeconomic Research Manager Jose Luis Mojica, drawing on data from SetFx, LSEG Workspace, the Banco de la República, the Departamento Administrativo Nacional de Estadística (National Administrative Department of Statistics) and JP Morgan.