Previous Story

Fitch Affirms Colombia At BBB- But Outlook Negative

Posted On January 18, 2021

Comment: Off

Fitch Ratings has affirmed Colombia’s Long-Term Foreign and Local Currency Issuer Default Ratings (IDR) at ‘BBB-‘ with a negative outlook. According to the ratings firm, Colombia’s ‘BBB-‘ rating reflects the government’s long track record of conservative macroeconomic policies that have underpinned macroeconomic and financial stability, but the ratings are constrained by high commodity dependence, weaker external metrics compared with peers, a rising government debt burden and structural weaknesses in terms of low GDP per capita and weaker governance indicators relative to peers.

The negative outlook reflects downside risks to the economic growth outlook and uncertainties about the capacity of the government’s policy response to decisively cut deficits and stabilize and eventually lower debt in the coming years, following the sharp rise in general government debt burden as a result of the coronavirus pandemic.

Fitch forecasts the economy to contract by 6.9% in 2020, broadly in line with the current BBB median of -6.7%, and rebound by 4.9% in 2021 given the severe lockdowns that negatively impacted domestic demand. Fitch projects growth of 3.8% in 2022, above the estimated medium-term growth potential of about 3.0% as a result of the large output gap that has emerged. However, the growth outlook for 2021 and over the medium term is highly uncertain given the rise in unemployment, potential closure of a number of businesses and uncertain dynamics of the pandemic.

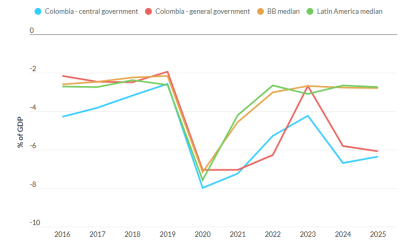

The central government fiscal deficit is forecast by Fitch to rise to 9.1% of GDP in 2020 due to the sharp fall in revenues and higher spending to combat the pandemic as well as economic reactivation measures. The deficit is expected to gradually diminish to 7.5% in 2021 and 4.9% in 2022. The government suspended its fiscal rule for two years to combat the pandemic and reactivate the economy with increases in spending in both years.

Although Fitch expects revenues to increase in 2021 given the cyclical economic rebound, income taxes and oil revenues will likely underperform the budget targets given lagged effects of 2020 economic activity and drop in oil prices. The ratings firm’s baseline assumption is for tax revenues to rise by around 2% of GDP in 2022-2024 due to implementation of a tax reform. On the spending side, we expect pandemic-related spending measures to taper off by 2022 as well as some cuts to capex. However, downside risks to Fitch’s fiscal projections are material.

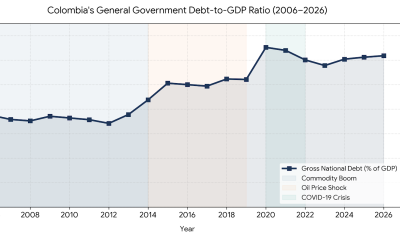

The general government debt to GDP is expected by Fitch to rise to 60.3% at YE 2020 (exceeding the forecasted BBB median of 52.7% of GDP) as a result of the large deficit, economic contraction and depreciation of the Colombian peso. Debt to GDP is expected to rise further over the next two years, although at a more gradual pace stabilizing at 62.6% of GDP in 2022 and then gradually fall. General government interest to revenues has also risen significantly to close to 13.2% in 2020 (above the current BBB median of 7.4%) from 10.8% in 2019.

Budget deficit reduction in 2022 will depend on the government’s ability to pass revenue-enhancing measures given the spending rigidities which regional transfers and other non-discretionary social spending impose. The government and fiscal council estimate 2% of GDP in additional revenue measures is required in its Medium-Term Fiscal Framework to begin to reduce the government debt burden.

President Duque’s relationship with the Congress has improved over the course of 2020, which could improve chances of tax reform. Furthermore, Colombia has a long track record of passing and implementing tax reforms over the last three decades (14 reforms), but they are often watered down in Congressional deliberations. Electoral considerations could complicate Colombia’s ability to pass difficult reforms. Congressional and Presidential elections are scheduled for March and May 2022, respectively.

Pension and labor market reforms could also possibly be introduced in 2021. The labor reform would seek to introduce flexibility into the rigid labor market, such as introduce contract labor and reduce high labor costs for businesses, which could improve economic growth prospects. Pension reform would seek to improve the system’s low coverage and replacement rates, which have been a source of social discontent.

The government financed the increase in the 2020 budget deficits largely from abroad, including the planned use of $5.3 billion USD from the IMF’s Flexible Credit Line. The foreign share of government debt has increased to nearly 40% from 34% in 2019.

Colombia’s current account has averaged 4% of GDP over the last 10-years given savings and investment trends, and despite the flexibility of the Colombian peso. However, FDI has covered around 70% of the current account deficit in the last decade, where it is expected to remain over the medium term. In 2020, the current account deficit has narrowed to an expected 3.5% of GDP, down from 4.3% in 2019. A fall in exports due in part to the fall in the average oil price will be compensated by the sharply contracting household consumption and investment suppressing imports. Furthermore, profit remittances have fallen. Fitch says that it expects the deficit to remain largely unchanged in 2021 in terms of GDP although higher in dollar terms, with both exports and imports rising.

Net external debt is expected to rise to 18.4% of GDP in 2020 (surpassing the current BBB median of 10.2%), up from 12.1% of GDP in 2019. International reserves have risen in 2020 to $57 billion USD, from $52.7 billion USD in 2019 improving external liquidity measures (10 months of current account payments, up from 7.6 months in 2019). Colombia’s floating FX regime and the IMF’s Flexible Credit Line (augmented to USD17.2 billion in September 2020) help mitigate external vulnerabilities.

Inflation and inflation expectations have fallen below the midpoint of the 3+/-1% inflation target. Since March 2020, the central bank cut interest rates by 250 bp to 1.75% given the large fall in economic output expected in 2020 as a result of the coronavirus pandemic. In addition to rate cuts, the bank has implemented a number of other measures to support domestic credit and smooth local market volatility – including outright purchase of government and local corporate debt. It has also intervened in the FX market through derivatives (both forwards and swaps).

ESG – Governance

Colombia has an ESG Relevance Score (RS) of 5 for both Political Stability and Rights and for the Rule of Law, Institutional and Regulatory Quality and Control of Corruption, as is the case for all sovereigns. With regards to World Bank Governance Indicators (WBGI), Colombia has a medium ranking in the 46.6th percentile, reflecting a track record of peaceful democratic transitions of power, a moderate level of rights for participation in the political process, moderate institutional capacity, established rule of law and a moderate level of corruption. However, Colombia scores especially poorly in the area of political stability and absence of violence.

Rating Sensitivities

Factors that could, individually or collectively, lead to negative rating action/downgrade:

- Public Finances–Failure to achieve a fiscal consolidation consistent with stabilization and subsequent reduction in government debt burden.

- Macroeconomic–Evidence that the coronavirus shock is having a persistent impact on growth prospects.

- External Finances–Widening in the current account deficit that leads to a significant further rise in the net external debt burden.

Factors that could, individually or collectively, lead to positive rating action/upgrade are:

- Public Finances–Implementation of fiscal consolidation measures, such as increase in tax revenues, consistent with debt stabilization and eventual reduction.

- Macroeconomic– Evidence that the pandemic has not had a material impact on medium term growth prospects.

- External Finances–Narrowing in the current account deficit that improves external debt and liquidity ratios.

Fitch’s proprietary SRM assigns Colombia a score equivalent to a rating of ‘BB+’ on the Long-Term Foreign Currency (LT FC) IDR scale.

Fitch’s sovereign rating committee adjusted the output from the SRM to arrive at the final LT FC IDR by applying its QO, relative to SRM data and output, as follows:

- Macroeconomic: +1 notch, reflecting Colombia’s record of prudent macroeconomic policies and a policy framework that has underpinned macroeconomic stability and supported resilience to shocks. It also offsets the deterioration of the GDP volatility variable in the SRM driven by the impact of the pandemic shock, which we believe will be temporary, and would otherwise add excess volatility to the rating.

Fitch’s SRM is the agency’s proprietary multiple regression rating model that employs 18 variables based on three-year centered averages, including one year of forecasts, to produce a score equivalent to a LT FC IDR. Fitch’s QO is a forward-looking qualitative framework designed to allow for adjustment to the SRM output to assign the final rating, reflecting factors within our criteria that are not fully quantifiable and/or not fully reflected in the SRM.

Best and worst case ratings scenarios

International scale credit ratings of Sovereigns, Public Finance and Infrastructure issuers have a best-case rating upgrade scenario (defined as the 99th percentile of rating transitions, measured in a positive direction) of three notches over a three-year rating horizon; and a worst-case rating downgrade scenario (defined as the 99th percentile of rating transitions, measured in a negative direction) of three notches over three years. The complete span of best- and worst-case scenario credit ratings for all rating categories ranges from ‘AAA’ to ‘D’. Best- and worst-case scenario credit ratings are based on historical performance. For more information about the methodology used to determine sector-specific best- and worst-case scenario credit ratings, visit https://www.fitchratings.com/site/re/10111579.

Key Assumptions

As of its latest Global Economic Outlook (GEO) in September, Fitch projects global real GDP to grow 5.2% in 2021 after contracting 4.4% in 2020. The average oil price is $45 USD in 2021 and $50 in 2022.

The principal sources of information used in the analysis are described in the Applicable Criteria.

ESG Considerations

Colombia has an ESG Relevance Score of 5 for Political Stability and Rights as World Bank Governance Indicators have the highest weight in Fitch’s SRM and are highly relevant to the rating and a key rating driver with a high weight.

Colombia has an ESG Relevance Score of 5 for Rule of Law, Institutional & Regulatory Quality and Control of Corruption as World Bank Governance Indicators have the highest weight in Fitch’s SRM and are therefore highly relevant to the rating and are a key rating driver with a high weight.

Colombia has an ESG Relevance Score of 4 for Human Rights and Political Freedoms as the Voice and Accountability pillar of the World Bank is relevant to the rating and a rating driver.

Colombia has an ESG Relevance Score of 4 for Creditor Rights as willingness to service and repay debt is relevant to the rating and is a rating driver, as for all sovereigns.

Unless otherwise disclosed in this section, the highest level of ESG credit relevance is a score of ‘3’. This means ESG issues are credit-neutral or have only a minimal credit impact on the entity, either due to their nature or the way in which they are being managed by the entity. For more information on Fitch’s ESG Relevance Scores, visit www.fitchratings.com/esg.