Previous Story

Colombia’s Natural Gas Reserves Have Collapsed 54% Since 2018, with No Floor in Sight

Posted On July 7, 2026

Comment: 0

Gas buffer gone; reserves halved, replacement rate turns negative.

Colombia’s energy security is eroding faster than most investors realize. According to the Informe de Recursos y Reservas (Resources and Reserves Report, IRR) 2025, published June 23, 2026 by the Agencia Nacional de Hidrocarburos (National Hydrocarbons Agency, ANH), the country’s proven natural gas reserves — technically designated Category 1P — have fallen to 1,717 billion cubic feet (Bcf), known in Colombia as Giga pies cúbicos (billion cubic feet, Gpc). That figure represents a 54% collapse from the 3,782 Bcf held at the end of 2018. It is not a cyclical dip. It is a structural deterioration that is accelerating, driven in significant part by a government that has made halting hydrocarbon development an explicit policy objective.

For investors and analysts tracking Colombia’s fiscal position, industrial competitiveness, and household energy costs, the IRR 2025 is a report that demands careful reading. What it shows is a country consuming its own energy inheritance — and doing so at a pace it is no longer replenishing.

Seven Years of Losses

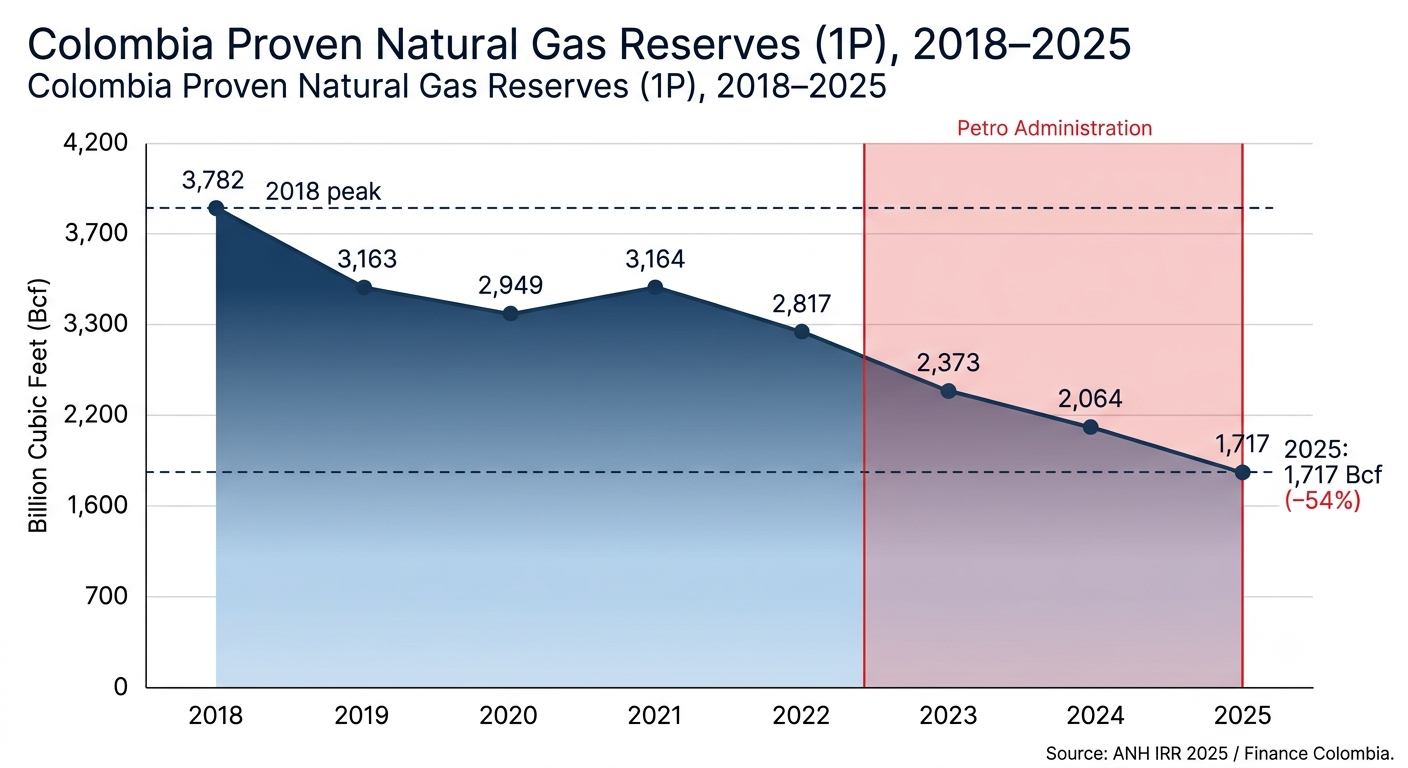

In 2018, Colombia held 3,782 Bcf of proven natural gas reserves. By the end of 2025, that figure had been cut nearly in half, to 1,717 Bcf. The 2025 result alone represents a drop of 347 Bcf compared to the 2,064 Bcf recorded at end-2024 — a single-year decline of 16.8%. Against the ten-year average of 3,259 Bcf, the current level is 47.3% lower.

What is striking about the annual trajectory is that the steepest declines have occurred since August 7, 2022 — the date President Gustavo Petro took office. Between 2018 and 2022, reserves moved within a range of 2,817 Bcf to 3,782 Bcf, fluctuating as production and new additions roughly balanced. Beginning in 2022, the trend turned sharply and consistently downward: 2,817 Bcf at end-2022, 2,373 Bcf at end-2023, 2,064 Bcf at end-2024, and 1,717 Bcf today. That is a loss of 1,100 Bcf in just three years.

The reserves-to-production (R/P) ratio — the industry’s standard measure of how many years of supply remain at current extraction rates — stood at 5.9 years as of December 31, 2025. Context: in 2007, when Colombia’s gas reserves reached their historical peak, the R/P ratio was 14.1 years. The current figure is 8.2 years below that peak, and 2.2 years below the ten-year average of 8.2 years. Put simply, at today’s production rate, Colombia would exhaust its proven gas reserves in under six years.

Graphic 1: Colombia proven natural gas reserves (1P, Bcf) 2018–2025.

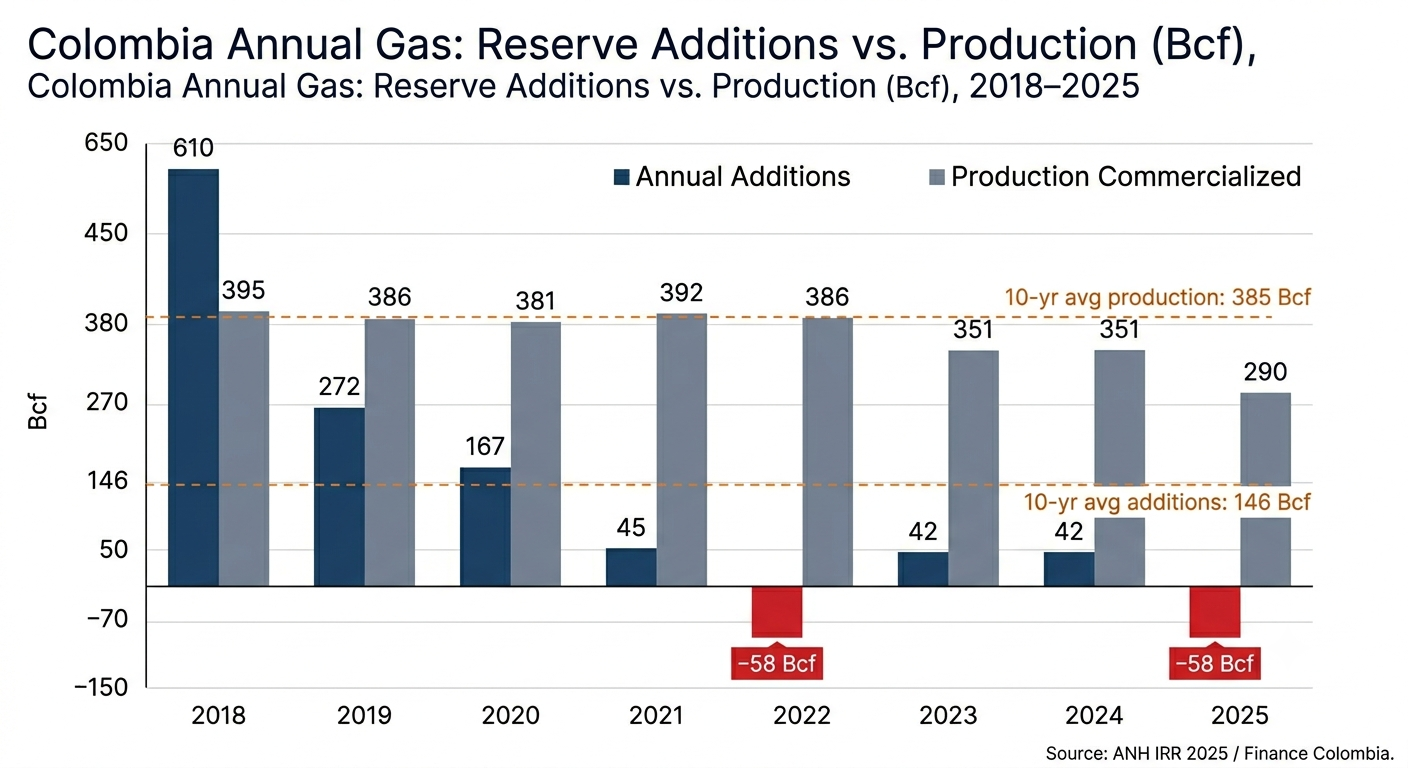

The Reserve Replacement Crisis

Reserves decline when production exceeds new additions. In 2025, Colombia’s total annual gas reserve additions reached negative 58 Bcf — meaning the country certified less gas than it extracted from the ground. This compares to positive additions of 42 Bcf in 2024, and a ten-year historical average of 146 Bcf per year in new additions. The 2025 figure is the worst annual result in the dataset.

The ANH’s reserve balance formula is straightforward: ending reserves equal starting reserves, minus production, plus total annual additions. With additions at -58 Bcf and production at 290 Bcf, the combined drain on reserves was 348 Bcf in a single year. The reserve replacement rate — which expresses additions as a percentage of production — stood at negative 20%, 32 percentage points worse than the replacement rate recorded in 2024.

“In 2024, Colombia lost its self-sufficiency and became dependent on foreign liquefied natural gas (LNG).” — El Colombiano, June 2026

A reserve replacement rate of negative 20% means that for every 100 cubic feet of gas Colombia produced in 2025, it certified negative 20 cubic feet of new supply. The industry considers a rate below 100% a warning sign. Colombia is now operating at negative territory.

The ANH identifies “technical revisions” — downward reinterpretations of existing field data — as the primary driver of the negative additions figure. Specifically, a downward revision of 125 Bcf from technical reassessments erased 60 Bcf in new discoveries and 5 Bcf in enhanced recovery additions, producing the net negative result. The revision reflects how mature Colombia’s major gas-producing fields have become. Over the last four years, the ANH notes, negative technical revisions have become a consistent pattern, “evidencing the high degree of maturity of the most representative gas fields in Colombia.”

The counterweight — new exploration discoveries — contributed 60 Bcf in 2025, a 62% increase over 2024 and the report’s most encouraging data point. In October 2024, Colombia announced its biggest gas discovery in four decades — a genuinely important find, though its contribution to 2025 additions illustrates that even large individual discoveries cannot compensate for the suppression of systematic exploration activity. It underscores that the remaining path to reserve growth runs through exploration, precisely the activity the Petro government has chosen to suppress.

Graphic 2: Annual gas reserve additions vs. production 2018–2025.

Production in Structural Decline

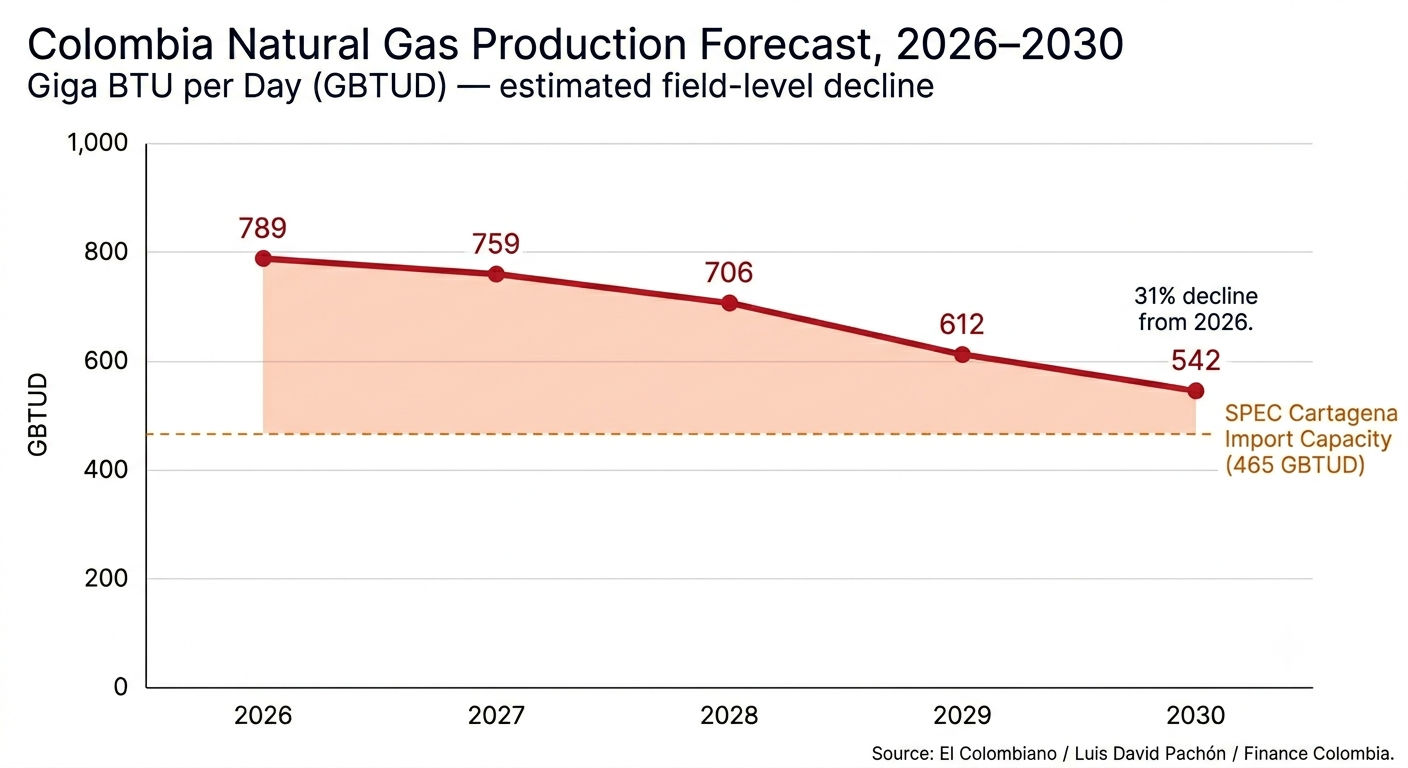

Gas production in 2025 came in at 290 Bcf — 61 Bcf less than the 351 Bcf commercialized in 2024, a reduction of 17.4%. Against the ten-year average of 385 Bcf per year, 2025 production was 95 Bcf below the historical norm.

The decline is not a one-year event. It is a trend line, and independent analysts say it will steepen. According to Luis David Pachón, energy and gas analyst and consultant quoted by El Colombiano in June 2026, Colombia’s average gas production potential in May 2026 was 789 Giga BTU por día (billion BTU per day, GBTUD). That represents a 7% drop from 848 GBTUD the previous year. Pachón’s estimates project a continued descent: 759 GBTUD in 2027, 706 GBTUD in 2028, 612 GBTUD in 2029, and just 542 GBTUD by 2030. That is a 31% decline from today’s already-reduced production level over five years.

These are not projections built on pessimistic assumptions. They are field-level extrapolations of what happens when existing reservoirs mature and no new supply is added. Without new exploration and development, this trajectory is, according to Pachón’s analysis, essentially locked in.

Graphic 3: Colombia gas production forecast 2026–2030 in GBTUD with SPEC import capacity reference line.

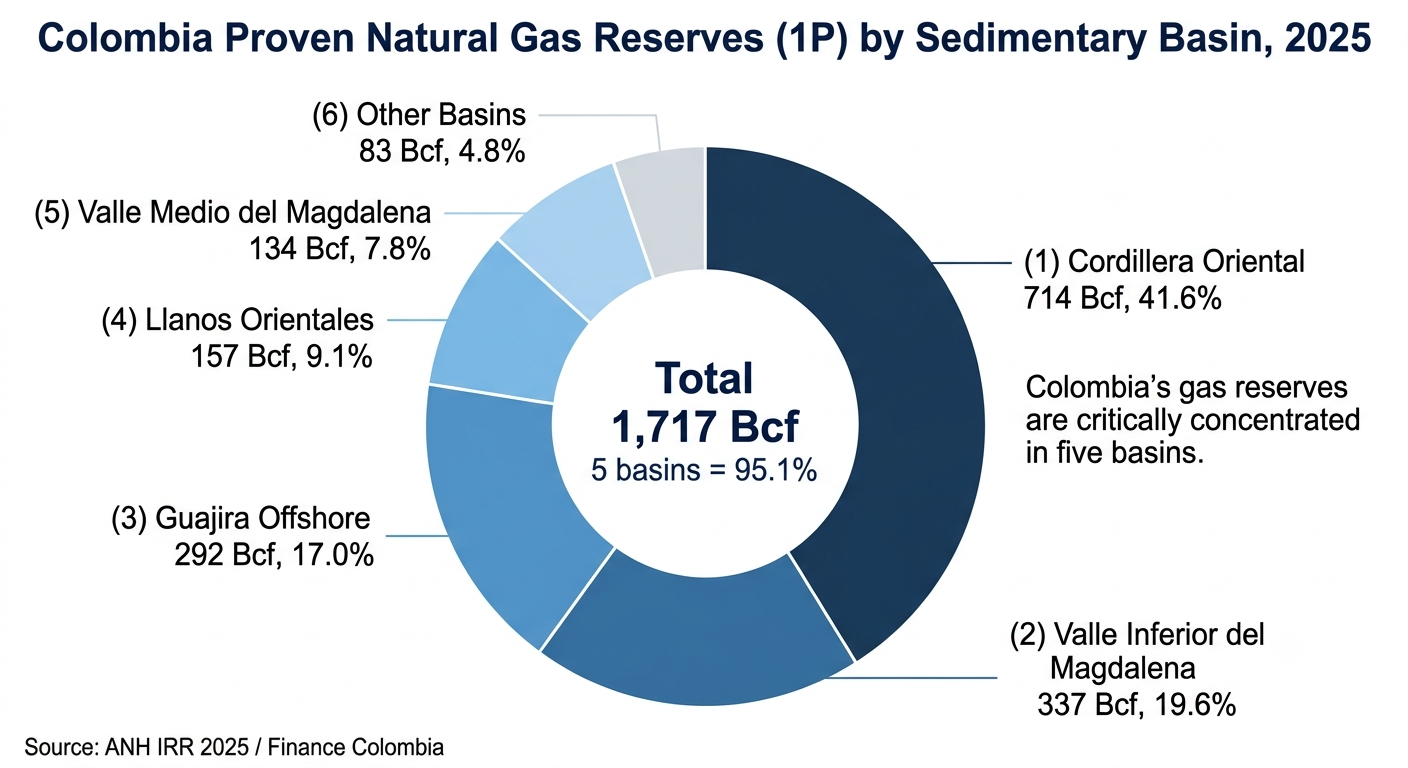

Geographic Concentration: A Portfolio with No Diversification

Colombia’s gas reserves are not only shrinking — they are dangerously concentrated. More than 95% of the country’s proven 1P gas reserves are held in just five sedimentary basins. The Cordillera Oriental leads with 714 Bcf, or 41.6% of the national total. The Valle Inferior del Magdalena holds 337 Bcf (19.6%), offshore Guajira contributes 292 Bcf (17%), the Llanos Orientales account for 157 Bcf (9.1%), and the Valle Medio del Magdalena adds 134 Bcf (7.8%). Together, these five basins hold 95.1% of Colombia’s proven gas reserves.

This concentration creates compounding risk. As the ANH’s own technical revisions confirm, the most mature fields driving those downward adjustments are concentrated in precisely these basins. A major operational disruption, regulatory interference, or accelerated depletion in any one of them would hit the national supply balance hard. Offshore Guajira’s 17% share is particularly relevant to watch, as it represents the primary frontier for future offshore development — development that the government’s moratorium on new contracts has deferred indefinitely.

Graphic 4: Colombia gas reserves 1P by sedimentary basin.

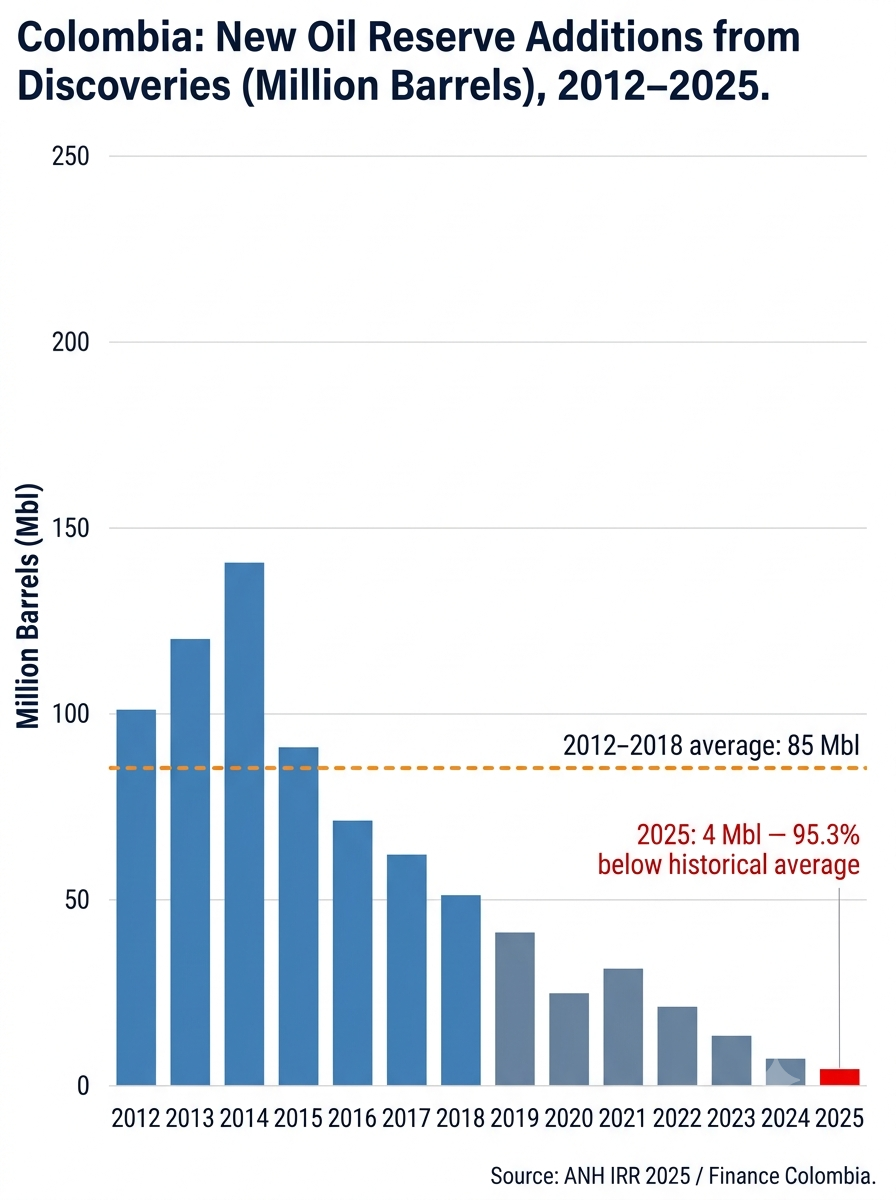

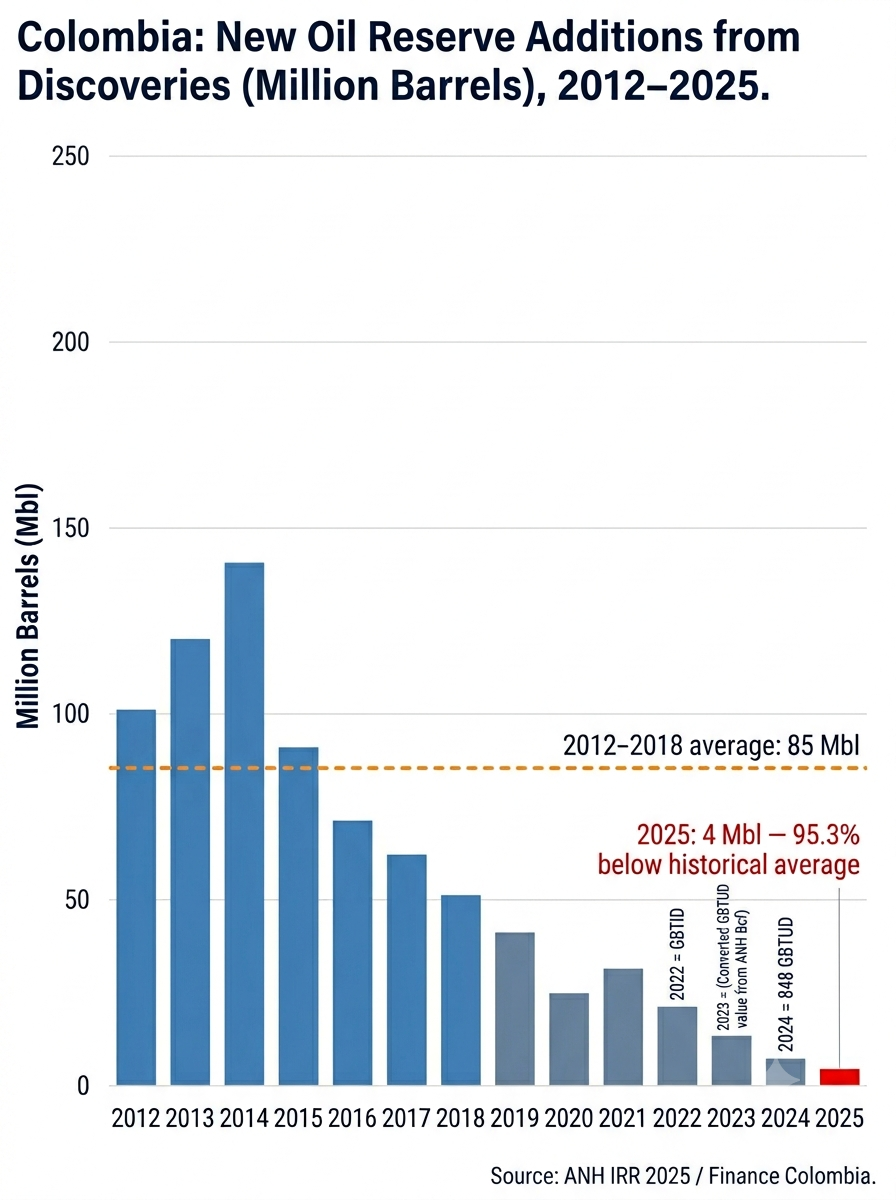

Oil Reserves: Stable on the Surface, Hollowed Out Below

Colombia’s proven oil reserves present a more stable picture at first glance. The country held 2,020 million barrels (Mbl) of 1P oil reserves at December 31, 2025, essentially unchanged from the 2,035 Mbl recorded in 2024 — a variation of -0.7%. The oil R/P ratio actually improved slightly, from 7.2 years in 2024 to 7.4 years in 2025, reflecting both effective field management through planes de producción incrementales (incremental production plans, PPI) and enhanced oil recovery (EOR) programs.

The ANH notes that between 2024 and 2025, PPI-EOR programs incorporated 58 Mbl into 1P reserves — 97% of the volume achieved the prior year, demonstrating that intensive management of existing fields is compensating, for now, for the near-complete absence of new exploration success.

But the stability in headline reserves conceals a critical vulnerability: the exploration pipeline is effectively empty. New oil reserve additions associated with discoveries — new wells finding new oil — reached only 4 million barrels in 2025. Between 2012 and 2018, the average was 85 million barrels per year in discovery-driven additions. That is a 95.3% collapse in exploratory success. When PPI-EOR programs exhaust their incremental potential in the medium term, there will be nothing in the exploration queue to replace them.

Colombia has 2,404 Mbl of contingent petroleum resources at the 3C level — discovered but not yet commercially viable — with 56% (1,358 Mbl) held back by environmental and social contingencies, and 20% (475 Mbl) blocked by unfavorable economics at current prices. The contingent resource base is real, but converting it to production requires investment, permitting, and a government that is not actively discouraging the industry. As Finance Colombia has reported, the Petro administration’s relationship with the hydrocarbon sector has been defined by hostility rather than partnership — a dynamic visible in Shell’s April 2025 exit from Colombian offshore gas projects, joining a parade of majors that have reduced or eliminated their Colombian footprint.

Graphic 5: New oil reserve additions from discoveries (Mbl) 2012–2025.

The Petro Factor: Policy as Accelerant

President Gustavo Petro has made the energy transition a defining banner of his administration. Within that framework, he has chosen not to sign new hydrocarbon exploration contracts — a policy decision with consequences that are now quantifiable in the IRR 2025 data.

The causal logic is not complicated: exploration today yields reserves in five to fifteen years. When exploration stops, the reserve pipeline runs dry on a predictable schedule. Colombia’s gas fields are mature. The industry has known for years that sustaining supply required either deepening work in existing concessions or opening new ones. Petro’s government has constrained both paths — by refusing new contracts and by creating a regulatory and political environment that has chilled investment in existing operations.

The ANH’s own report acknowledges the dynamic indirectly. It highlights that EOR project filings increased 82% comparing the 2020–2022 period to 2023–2025, which it presents as evidence of productive government measures. But this increase reflects the industry pushing harder on existing fields precisely because new exploration is not an available avenue — a compensatory reaction to policy constraint, not evidence that the policy is working. Even Ecopetrol (BVC: ECOPETROL, NYSE: EC), the state-controlled oil company whose board the Petro administration increasingly controls, has had to navigate the tension between engineering reality and the government’s anti-hydrocarbon posture; as far back as 2023, Ecopetrol’s then-new president was publicly advocating for more exploration in direct opposition to Petro’s stated goals.

The Asociación Colombiana del Petróleo y Gas (ACP) has consistently warned that without new exploration contracts, Colombia’s hydrocarbon production would follow a predictable decline curve. The IRR 2025 confirms those warnings with data. The reserves trajectory under Petro — from 2,817 Bcf at end-2022 to 1,717 Bcf today — is the most direct measure available of what a no-new-contracts policy costs in energy security terms.

Import Dependency: An Avoidable Humiliation

The practical consequence of reserve depletion is playing out in real time at Colombia’s gas import terminals — and in consumers’ utility bills. Finance Colombia reported in March 2025 that Bogotá’s Vanti had already raised gas rates 36% and Medellín’s EPM by 21%, with the deficit cited as the direct cause. In 2024, Colombia lost its natural gas self-sufficiency for the first time and began depending on imported liquefied natural gas (LNG) to meet domestic demand — a fact reported by El Colombiano in June 2026. The situation deteriorated further: in the first week of June 2026, 32% of all gas consumed in Colombia came from imports through the regasification plant in Cartagena, operated by Sociedad Portuaria el Cayao (SPEC). That is the highest import share in the country’s history, according to data from the Sistema Electrónico de Gas (Electronic Gas System).

SPEC’s Cartagena facility has an import capacity of 465 GBTUD. Approximately two-thirds of that capacity is already being utilized to serve national demand, leaving a shrinking fraction available to absorb any additional supply shortfall. Given the production decline trajectory outlined by Pachón — down to 542 GBTUD by 2030 — Colombia will require significantly more import capacity than it currently has, or it will face supply rationing.

Additional regasification projects are under development — in Buenaventura, Coveñas (Sucre), and Ballena (La Guajira), in addition to the operating Cartagena facility. These are necessary investments. But they are investments in the infrastructure of dependency: Colombia building the capacity to pay other countries for gas it has in its own subsoil but has chosen not to extract.

The distributional consequence deserves to be stated directly. Over the past two decades, access to natural gas transformed household energy use for millions of lower-income Colombians, displacing wood combustion in cooking and heating. Wood burning accelerates deforestation, degrades air quality, and imposes a disproportionate burden on households that cannot afford cleaner alternatives. A policy that drives Colombia back toward LNG import dependency — at premium prices — is a policy that will price gas out of reach for those same households, potentially reversing one of the country’s most concrete environmental gains. Cheaper domestic gas served the poor. Expensive imported LNG will not.

Graphic 6: Gas production decline vs. growing import share / SPEC capacity.

Contingent Resources: The Potential That Policy Cannot Unlock

There is one genuinely encouraging number in the IRR 2025: Colombia holds 10,540 Bcf of contingent gas resources at the 3C level — discovered, potentially recoverable volumes that are not yet classified as commercial reserves. Of that total, 7,855 Bcf (74.5%) sits offshore, with the remaining 2,685 Bcf onshore. Offshore resources are more than twice the onshore total, consolidating the offshore Caribbean as Colombia’s primary future supply option.

The obstacle is not geology. Of the 10,540 Bcf in contingent gas resources, 55% (5,818 Bcf) is held back by environmental and social contingencies — primarily offshore licensing processes, consulta previa (prior consultation), and community negotiations. Another 29% (3,037 Bcf) is blocked by legal and contractual contingencies, including the unresolved regulatory framework governing connections to the national transport system for offshore production. Only 9% is technically constrained.

The ANH has identified acceleration of environmental licensing for the offshore Sirius project as a priority measure for 2026. That is a constructive step. But accelerating the licensing of a single project does not substitute for the policy framework that would enable the industry to develop this contingent resource base systematically. The government’s refusal to sign new exploration contracts means the 10,540 Bcf of contingent offshore gas will remain contingent for the foreseeable future — a frustration the industry has tracked for years, as Finance Colombia documented as early as 2023 when a second consecutive failed tender for Pacific region gas infrastructure signaled the depth of the supply challenge.

Fiscal Implications for Investors

The royalty trajectory is one of the clearest financial signals in the IRR 2025. Since August 7, 2022, through December 31, 2025 — a 40-month window spanning the Petro administration — cumulative hydrocarbon royalties reached COP 29.6 trillion, averaging COP 0.74 trillion per month. The ANH projects that the existing 1P proven reserves, valued at current prices, will generate an additional COP 36 trillion in royalties over their remaining life.

That COP 36 trillion projection is not a guarantee. It assumes production continues at roughly current rates, that prices hold, and that the reserves are fully extracted. Given the R/P ratio of 5.9 years for gas and 7.4 years for oil, and given the absence of new exploration, the royalty stream is finite in a way it was not five years ago. Colombia’s fiscal planners and subnational governments that depend on hydrocarbon royalty transfers should be building their budgets around a declining baseline, not a stable or growing one.

For international energy investors, the picture is one of attractive geological potential — 10,540 Bcf of contingent gas resources, 2,404 Mbl of contingent oil — combined with a policy and regulatory environment that has made converting that potential into production exceptionally difficult. As the ANH has noted, the EOR and PPI programs within existing contracts are producing results. But those programs work within existing concessions. Without new exploration acreage, they are rearranging deck chairs on a ship whose fuel is running out.

The Petro administration ends in August 2026. What the next government inherits is not a blank slate: it inherits a reserve base that will take a decade of sustained investment to rebuild, import infrastructure sized to a new dependency it did not choose, and a domestic industry that has spent four years under sustained policy pressure. The IRR 2025 is the most comprehensive accounting yet of what that pressure has cost.

Finance Colombia has covered the evolution of Colombia’s hydrocarbon sector, gas supply outlook, and energy transition policy in depth. For related coverage see: Shell Exits Colombian Offshore Gas Projects (April 2025); Colombia Braces for Surging Energy Costs as Natural Gas Deficit Expands (March 2025); and Petro Administration Announces Natural Gas Rationing Despite Abundant Hydrocarbon Resources (October 2024). Additional technical data is available directly from the ANH at anh.gov.co.